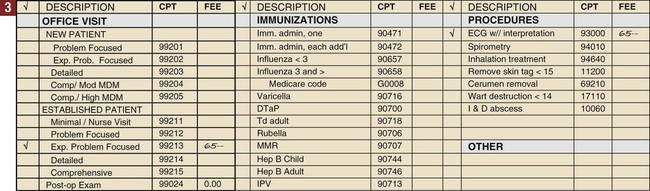

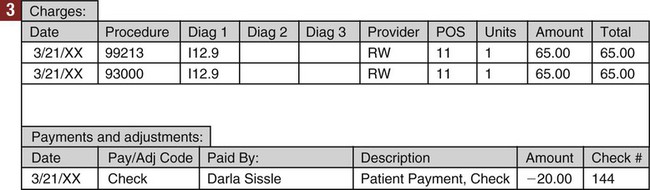

• A daily journal, commonly called a day sheet, to record all transactions that occurred on that day. • An accounts receivable ledger for each patient, to keep a record of transactions related to that patient. • A cumulative record of financial activity for the month, both for the practice as a whole and for each individual physician; this information is recorded on the day sheet, and cumulative totals are carried forward throughout the month. Highlight on Bookkeeping Systems Single-entry bookkeeping system The single-entry bookkeeping system is the simplest system. It requires at least three records: 1. A chronologic journal that keeps track of all charges and patient payments, such as a daily journal. 2. A journal that keeps track of payments made by the medical office, traditionally a checkbook but now usually an electronic check register. 3. A method to keep track of individual patient accounts; these used to be recorded on pages of a book, index cards, or ledger cards, but today they are usually accounts in a computerized billing program. In traditional medical office manual accounting systems, a “one-write” or “write-it-once” system (also called a pegboard system) is used. All necessary forms are held in place on a metal or plastic board by a row of pegs across the left side. In this type of system, information from the top form is transferred to the forms below. Entering information once generates a charge slip and receipt, an entry on the patient’s ledger card, and an entry on the daily journal (day sheet) (Figure 44-1). Although simple charge slips are still sometimes used, most medical offices use a customized superbill as a charge slip. The top section of the form is filled out with patient information by using a printed label, filling it out manually, or printing the information on the form from the computer. Figure 44-2 shows an example of a completed superbill. A fee schedule is a list of charges for the various procedures a physician performs. Years ago, a physician had one set of fees that he or she charged patients for office visits, procedures, and/or treatments. Today, however, a medical practice may have to accept different amounts as payment for each service it performs, depending on which insurance provider is paying for the service. The reimbursement varies from a fixed percentage of the physician’s charges to a set amount for a given service. Insurance is discussed in detail in Chapter 46. The medical office usually has a basic fee schedule, listing the usual charges for office visits and procedures. The fee schedule is used to fill out charges on the charge slip or superbill. When a computer billing program is used, the amount charged for each procedure is linked to the procedure and usually comes up automatically when the correct procedure is selected. Most computer billing programs can link a patient’s fees to his or her specific insurance fee schedules, such as Medicare and Medicaid (Procedure 44-1). Complete an itemized charge slip for a patient using a fee schedule. 1. Procedural Step. Before the patient is seen by the physician, complete the top part of an itemized charge slip with the information requested including the patient’s name, date of birth, insurance, insurance group, and subscriber numbers and the name of the subscriber (insured person). This may be done manually from information on a ledger card or computer account, by attaching a label printed by the computer, or by printing charge slips using the computer billing program. 2. Procedural Step. Before the patient is seen by the physician, enter the patient’s previous balance on the bottom of the charge slip. 3. Procedural Step. Using the fee schedule, fill in the charges on the charge slip by writing the fee for each service provided beside the line containing the correct code and procedure name (if the physician has not already done so). 4. Procedural Step. Complete the remainder of the charge slip by entering the total charges and payment made, and then calculate the new balance. The new balance is the sum of the total charges and previous balance minus any payment. 5. Procedural Step. Complete other information requested on the charge slip, such as the place of service and check number and/or method of payment. Each patient has his or her own account. It is important to verify that all information about the account is current when the patient arrives at the office, because address information and insurance information can change between visits. A cumulative record of charges and payments is kept, usually using a computer program. It is also possible to keep account records manually. This record of charges and payments is called the patient account ledger. In a computer billing program, the patient account ledger is linked to the patient demographic and insurance information so that periodic bills and insurance claims can be generated. Information about services provided to an individual patient and payments received for that patient show up in chronologic order on the patient ledger (Figure 44-3). After the charge slip has been completed, the charges are posted to the patient ledger (Procedure 44-2). Procedure 44-2 Posting Charges Using the information from the completed charge slip, post patient charges to a patient account. 1. Procedural Step. If using a manual system, post the charges from a completed patient charge slip on the patient ledger using one line for one day’s services. Place the total charges for the services in the column labeled “charges.” If using a computer program, post the first charge on the first line of the transaction entry screen. For most computer programs, entering the procedure code will prompt the computer to automatically generate the correct charge for the patient’s insurance. 2. Procedural Step. If using a computer system, post each additional charge on a new line. 3. Procedural Step. If using a manual system, enter the total charge in the balance column. If using a computer system, save your work after all charges have been posted. Payment for services performed can be received in four ways: 1. The patient pays at the time of service, in full, or in part (e.g., a copayment for managed care insurance). The office will accept cash and checks, and most offices also accept credit and debit cards. 2. The patient may make a payment through the mail in response to a bill. 3. The patient may make an online payment using a credit or debit card through the medical practice website. 4. An insurance company may make a payment either by mail or, increasingly, by electronic transfer. A change to the patient account that is neither a charge for services nor a payment is called an adjustment. Credit (negative) adjustments are subtracted from the patient balance. Examples of credit adjustments include discounts for payment at the time of service, professional courtesy, and discounts given to insurance companies (also called insurance write-offs). Credit adjustments are usually discounts that are given in specific circumstances. (See Box 44-1 for common terminology used in accounting.) Debit (positive) adjustments are added to the patient balance. Debit adjustments will be discussed in more detail in Chapter 47. When using a computer billing program, the medical assistant selects a code for each charge, payment, or adjustment. The correct mathematical operation is linked to the transaction code so that the computer automatically adds charges and debit adjustments (such as a returned check) to the patient balance and subtracts payments and credit adjustments (such as an insurance write-off). (Procedure 44-3). Procedure 44-3 Posting Payments and/or Adjustments Post payments and/or adjustments to a patient account. • Patient ledger card or computer • Check or cash from the patient or payment from the insurance carrier • Stamp with restrictive endorsement 1. Procedural Step. When a payment has been made, locate the patient account in the computer or select the patient ledger card. 2. Procedural Step. Compare the amount of the payment against the total amount owed. Principle. The total amount owed will be the balance due and charges for new services. 3. Procedural Step. If using a manual system, post the payment from a completed patient charge slip on the patient ledger on the same line as the day’s charges. If it is a check, record the number of the check. If using a computer program, post the patient payment on the same screen as the charges from the day’s visit. Use the appropriate payment code for cash or check when entering the payment.

Managing Practice Finances

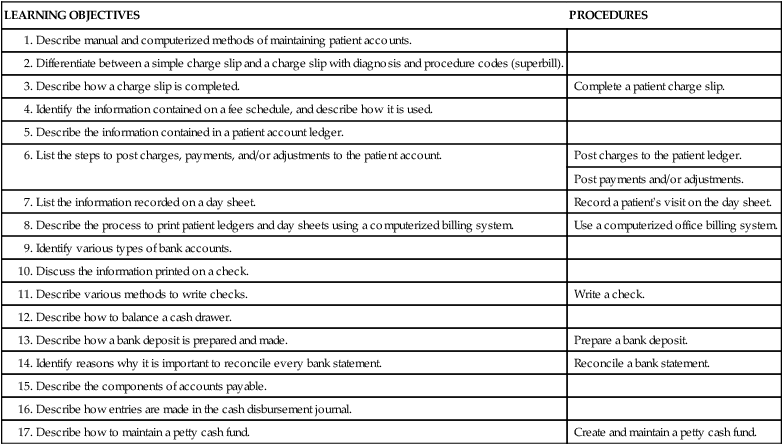

LEARNING OBJECTIVES

PROCEDURES

Complete a patient charge slip.

Post charges to the patient ledger.

Post payments and/or adjustments.

Record a patient’s visit on the day sheet.

Use a computerized office billing system.

Write a check.

Prepare a bank deposit.

Reconcile a bank statement.

Create and maintain a petty cash fund.

Introduction to Daily Financial Activities

Maintaining Patient Accounts

Components of A Patient Account

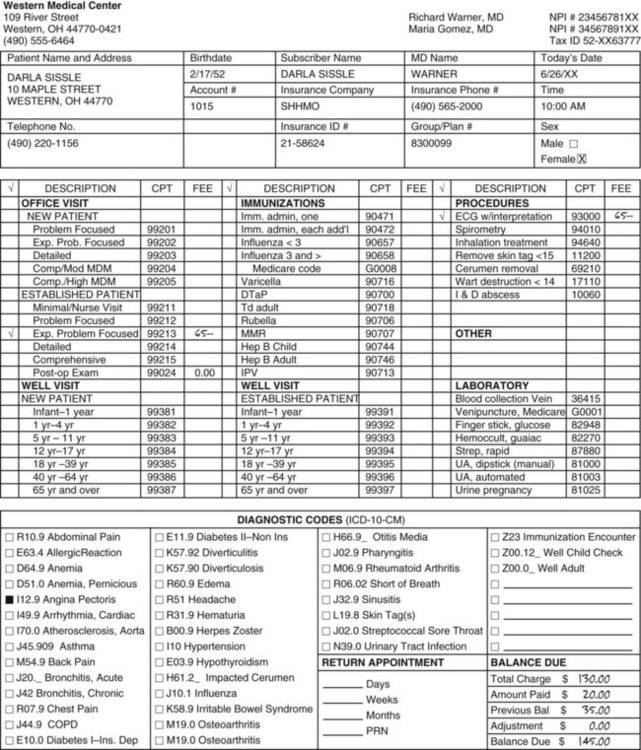

Charge Slip

Fee Schedule

Procedure 44-1 Completing a Patient Charge Slip

Procedure 44-1 Completing a Patient Charge Slip

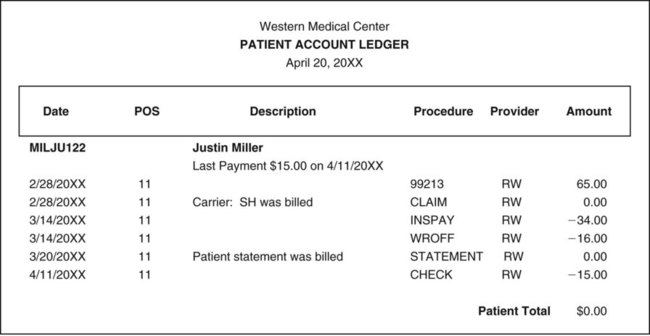

Patient Account Ledger

Posting Payments to the Patient Account

Posting Adjustments to the Patient Account

![]()

Stay updated, free articles. Join our Telegram channel

Full access? Get Clinical Tree

Managing Practice Finances

Get Clinical Tree app for offline access