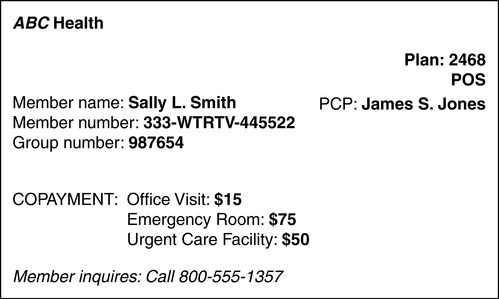

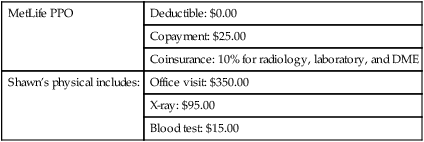

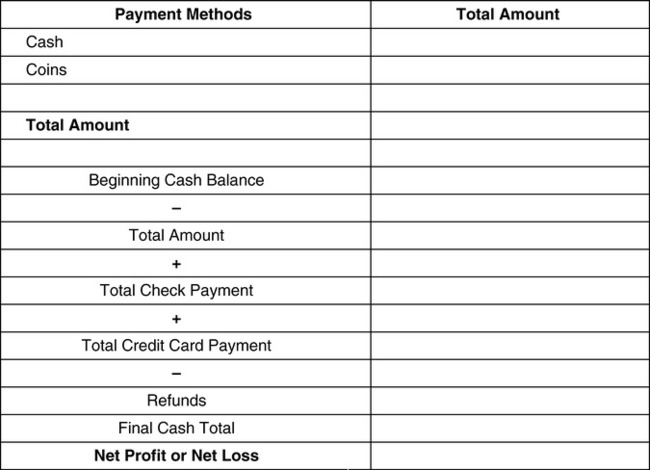

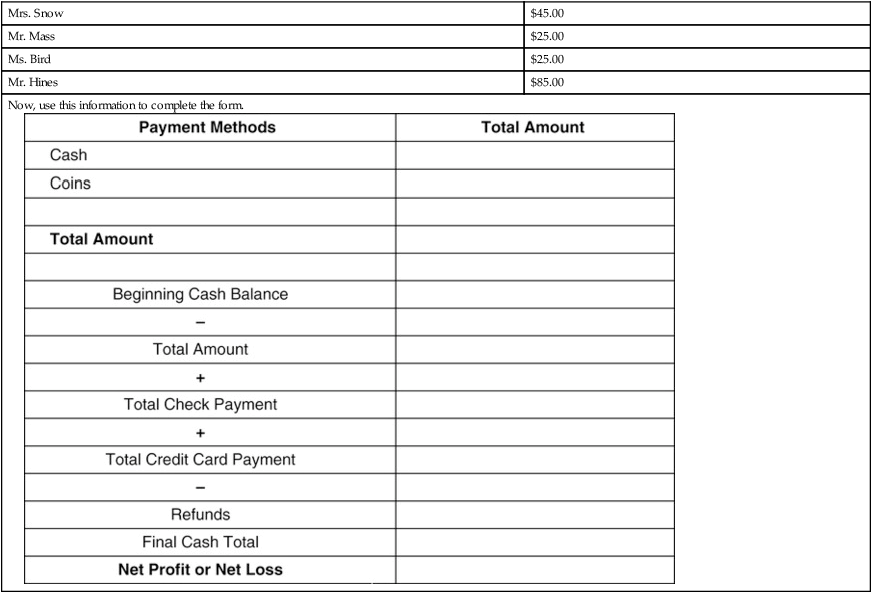

Upon completion of this chapter, the learner will be able to: 1. Define the key terms that relate to the chapter. 2. Identify key terms within a word problem and record information with 100% accuracy. 3. Manipulate word problem information with 100% accuracy. 4. Calculate insurance deductibles and copayments with 100% accuracy. 5. Analyze and balance day sheet information with 100% accuracy. 6. Calculate and record petty cash transactions with 100% accuracy. 7. Manipulate tax information to determine gross and net pay with 100% accuracy. Mr. Ford has insurance from his employer (primary), and he is also covered under his wife’s policy (secondary). When Mr. Ford is seen by the physician, the primary insurance company will pay 90% for the usual and customary services. Then, instead of Mr. Ford paying the remaining 10%, it is submitted to his wife’s insurance company for payment. Identify whether coinsurance, copayment, or a deductible would be collected based on the question 1. Mrs. Smith’s insurance policy requires her to pay $25.00 every time she visits the physician’s office. Mrs. Smith has a ____________________________. 2. Mr. Stone has an appointment on January 5, 20XX. He has Medicare Part B insurance, which requires him to pay a specified amount at the beginning of each year before the insurance coverage begins. This is an example of a _________________________. 3. Mr. Auburn has private insurance through Blue Cross/Blue Shield. He is required to pay 20% of all services performed when he sees the physician. This is an example of _________________________. 4. Mrs. Candle is required to pay $110.00 at the beginning of each year before her insurance coverage begins. After the $110.00 is collected, she is required to pay 10% of all services performed. Mrs. Candle does nothave to pay a ________________________ ________________________. 5. A ______________________, if required, is usually collected before the patient sees the physician. 6. _____________________ is commonly collected at the end of the visit. 7. Medicare Part B states that a patient will pay 80% of the usual and customary charges after the ________________________ has been met. 8. Mary Smith has an appointment to see Dr. Drake. She must pay her ____________________ before her insurance coverage will become effective. 9. Private insurance traditionally requires both a _________________ and a ________________________. 10. Managed care plans require a _________________to be paid at the time of each visit. 1. Look at the insurance card in Figure 6-1. 2. Determine if the insurance plan has a copayment amount (copay). 3. Collect the copayment amount. 4. Record collection of fees as described later in the chapter. Remember: this amount is not deducted from the total amount of the bill. 5. Copayments are collected every time the patient is seen by the physician; this includes follow-up visits. Refer to Figure 6-1 and answer the following questions 1. Does the card indicate that the patient has hospital coverage? _____________________________ 2. Does the card indicate that the patient has a primary care physician? __________________________ 3. Is there a different copayment amount for urgent care or emergency room visits? ___________________________ 4. What is the copayment amount for the emergency room, if indicated? __________________________ 5. What is the copayment amount for an office visit, if indicated? _____________________ 6. What is the copayment amount for an urgent care visit, if indicated? __________________________ 1. Contact the insurance company or the designated secure website to determine if a deductible has been paid in full. If not, what portion of the deductible has been met? 2. Depending on the policy of the facility, you may be required to collect a portion of the deductible before the patient sees the physician. Alternatively, the deductible may be collected at the end of the visit once the total amount of the bill has been determined. 3. Properly document how much of the deductible was collected. This information must be turned in to the insurance company to determine when coverage will begin. 4. Subtract the amount of the deductible from the total bill to determine the billable amount. 5. Record collection of fees as described later in the chapter. Mr. Ryan’s insurance policy has a $250.00 per year deductible. On January 13, 20XX, Mr. Ryan is seen in the physician’s office. His bill totals $185.00. This is the first time he has used his health insurance this year. Answer the following questions based on this scenario. 1. What is the total amount of Mr. Ryan’s yearly deductible? ___________________ 2. How much has been met this year toward the deductible? ____________________ 3. How much should you collect from Mr. Ryan toward his deductible? __________________ 4. Has Mr. Ryan met his deductible for the year? ________________________ If not, how much will he need to pay before his insurance becomes active? ________________________________ 1. Contact the insurance company, either by phone or on a secure website, to determine if the patient has coinsurance. 2. Find out whether there is a deductible and how much has been met. (Remember: the deductible must be met before insurance coverage begins.) 3. Verify the insurance company’s responsibility for the bill and the patient’s responsibility for the bill. (The total amount cannot equal more than 100%.) 4. Once the total bill has been established, determine the patient’s responsibility. (If you have forgotten how to determine percentage, refer to Chapter 4.) 5. Collect the amount for which the patient is responsible at the end of the visit. 6. Subtract the amount of the coinsurance from the total bill to determine the billable amount. 7. Record collection of fees as described later in the chapter. Determine the patient’s responsibility in each of the following problems 1. You have verified that the insurance company’s responsibility is 65%. a. What is the patient’s responsibility? ______________________ b. If the total bill for this visit is $65.40, how much will you collect from the patient? _____________________________ c. How much will you bill the insurance company? ___________________ 2. You have verified that the patient’s responsibility is 20%. 1. Contact the insurance company either by phone or on a secure website to determine if the patient has coinsurance. 2. Find out whether there is a deductible and how much has been met. 3. Verify the insurance company’s responsibility for the bill and the patient’s responsibility for the bill. 80/20 80% Insurance/20% Patient 4. Determine the total amount of the bill. 5. First, subtract the outstanding deductible from the total bill to determine the billable amount. $425.00 – $150.00 = $275.00 billable amount 6. Next, determine what percentage of the billable amount is the patient’s responsibility. $275.00× 20% = $55.00 is the patient’s responsibility 7. Determine the total amount that will be collected from the patient. $150.00 + $55.00 = $ 205.00 will be collected from the patient 8. Record collection of fees as described later in this chapter. 1. Check the insurance card to determine whether there is a copayment and the amount. Contact the insurance company either by phone or on a secure website to find out whether the patient has coinsurance for radiology, laboratory, or durable medical equipment (DME). 2. Depending on the policy of the facility, collect the copayment before the patient sees the physician. If x-rays, laboratory work, or DME is a possibility, your facility might have you collect the total amount at the end of the visit. 3. At the end of the visit, determine whether the coinsurance would apply toward any procedures. Lab fee: $15.00; x-ray fee: $92.00 Total coinsurance amount: $107.00 4. Determine the patient’s coinsurance responsibility. 5. Subtract the coinsurance amount from the total bill to determine the billable amount. Total bill $230.00– $26.75 = $203.25 6. Determine the total amount that will be collected from the patient. 7. Record collection of fees as described later in this chapter. Answer the following questions based on the information provided in the word problems 1. Mr. Smith has Medicare Part B insurance. Medicare has a $134.00 yearly deductible. Once the deductible has been met, the coinsurance coverage is 80/20. This is the first visit of the year for Mr. Smith. His total bill is $95.00. a. What is the total amount of the yearly deductible? ________________ b. How much should you collect from Mr. Smith? __________________ c. Has Mr. Smith met his yearly deductible? If not, what is the remaining balance? ______________________________________ d. Mr. Smith has not met his yearly deductible. How much will you collect? ______________________________________ e. Will Mr. Smith have to pay coinsurance? If so, how much? ______________________________________ f. What is the total amount you will collect from Mr. Smith? ________________________ g. What is the total billable amount for this visit? ___________________ 2. Shawn has scheduled an appointment for a complete physical. He has the following insurance: He is to return in 10 days for the test results. a. What is the copayment amount? _______________________________ b. What other amount will you collect? ___________________________ c. How much will you collect when the visit is over? _________________ d. How much should you collect for this visit? _____________________ e. When will you typically collect this fee? _________________________ 1. Terri comes into the physician’s office for a follow-up visit regarding her asthma. Her insurance has a $25.00 copayment. The total charge for Terri’s visit today is $65.00. How much will you collect from Terri? _______________________________________________ 2. Tom falls off his ladder at home. He is seen in the emergency room for a fractured tibia. He has 85/15 coinsurance. The total emergency room expenses are $1015.00. How much will you collect from Tom? ______________________________________ 3. Mary Elizabeth has Medicare Part B. Medicare requires a yearly deductible of $124.00. After the deductible has been met, Medicare’s coinsurance is 80/20. Mary Elizabeth has paid $72.50 toward her deductible. Today’s bill is $135.00. a. How much will you collect from Mary Elizabeth? _______________ b. How much will you bill Medicare? ____________________________ 4. Martin’s HMO plan has a $20.00 copayment for office visits. The insurance covers 80% of all x-rays and laboratory procedures. Martin is seen for a dislocated shoulder. He is charged the following fees: office visit $115.00 and x-ray $92.00. a. How much will you collect from Martin? ________________________ b. How much do you expect the insurance company to pay? _____________________ 5. Mr. Stephen has both Medicare and MetLife insurance. Medicare has a $124.00 yearly deductible of which he has paid $98.80. After the deductible has been paid, Medicare will pay 80%. MetLife will not pay for any expenses until the Medicare deductible has been met; they will then pay up to 20% of any fees not covered by Medicare. Mr. Stephen is being seen by a cardiologist and incurs the following charges: a. How much will you collect from Mr. Stephen? ____________________ b. How much will you bill Medicare? ______________________________ c. How much will you bill MetLife? _______________________________ 6. Your physical therapy visit cost $150.00. The insurance will cover 75% of the bill. How much will you need to pay? ________________________ 7. Fred was hospitalized for 6 days. His insurance has a $150.00 deductible for days 1 to 3 and then will pay 80% of the usual and customary charges. a. Expressing your answer as a formula, estimate the amount you expect Fred to be billed. _________________ b. Expressing your answer as a formula, estimate the amount you expect the insurance company to pay toward Fred’s bill. ________________ 8. Your employer requires you to get a physical. This is not a benefit covered by your insurance carrier. The physical costs $65.00. According to your insurance card, you have a $30.00 copayment for all office visits. How much would you expect to pay for the physical? _____________________ 9. Mary Jane’s primary insurer is a PPO, and her secondary insurer is MetLife. The insurance companies have established that the PPO will pay 70% of all medical expenses. Mary Jane has a $20.00 office visit copayment. a. How much will you collect from Mary Jane? ______________________ b. How much do you expect the PPO to pay? _______________________ c. How much do you expect MetLife to pay? ________________________ 10. Your insurance will pay 60% of all DME. Because of an accident, you must buy a knee immobilizer for $55.00 and a set of crutches for $27.50. Many facilities use a cash drawer worksheet similar to the one on p. 131. The purpose of this worksheet is to accurately document all currencytransactions involving the cash drawer throughout the day. It is essential to have documentation of the beginning balance of your cash drawer at the start of each day. 1. Determine the amount in your cash drawer before the start of business. Write this amount down and place your tally in a reliable location. 2. Count each form of currency. Write down the total number of bills and the total cash amount. 3. Add the total amount of all coins. 4. Subtract the total amount of currency at the end of the day from your beginning balance. This is your net profit. 5. Record all credit card and debit card transactions. Add to the total cash balance. 6. Record any checks received as payment. Add to the total cash balance. 7. Record any refunds. Subtract from the total cash balance. At the start of business, your cash drawer has a total of $375.00. At 3:30 p.m., your shift is ending and you must balance the cash drawer. Based on the following information, complete the form below and determine the total net profit for your shift. At the end of your shift, the following is in your cash drawer: Denomination Number of bills and coins $50.00 bills 2 $20.00 bills 17 $10.00 bills 4 $5.00 bills 25 $1.00 bills 40 $1.00 coins 0 Half dollars 0 Quarters 13 Dimes 17 Nickels 5 Pennies 13 Finally, the office manager authorized the following refunds to be paid from your drawer: Use the following worksheet to answer the questions.

General Accounting

Objectives 1, 2

Insurance

Objectives 3, 4

Collecting Copayment, Deductibles, and Coinsurance

STRATEGY 6-1

STRATEGY 6-1

Determining Copayment Amounts

STRATEGY 6-2

STRATEGY 6-2

Determining Deductible Amounts

STRATEGY 6-3

STRATEGY 6-3

Determining Coinsurance Amounts

STRATEGY 6-4

STRATEGY 6-4

Determining Deductibles and Coinsurance

STRATEGY 6-5

STRATEGY 6-5

Copayment and Coinsurance Combination

MetLife PPO

Deductible: $0.00

Copayment: $25.00

Coinsurance: 10% for radiology, laboratory, and DME

Shawn’s physical includes:

Office visit: $350.00

X-ray: $95.00

Blood test: $15.00

BUILDING CONFIDENCE WITH THE SKILL 6-1

BUILDING CONFIDENCE WITH THE SKILL 6-1

Office visit

$95.00

EKG

$45.00

Laboratory test

$35.00

Objectives 5, 6

Cash drawer, day sheets, ledger cards, and petty cash

Cash Drawer

STRATEGY 6-6

STRATEGY 6-6

Balancing a Cash Drawer

Credit cards:

$135.00

Checks:

$1030.62

Mrs. Snow

$45.00

Mr. Mass

$25.00

Ms. Bird

$25.00

Mr. Hines

$85.00

Now, use this information to complete the form.

Denomination

Number of bills and coins

$50.00 bills

2

$20.00 bills

7

$10.00 bills

14

$5.00 bills

15

$1.00 bills

24

$1.00 coins

0

Half dollars

3

Quarters

10

Dimes

7

Nickels

15

Pennies

23 ![]()

Stay updated, free articles. Join our Telegram channel

Full access? Get Clinical Tree

MATH IN THE REAL WORLD 6-1

MATH IN THE REAL WORLD 6-1 MATH IN THE REAL WORLD 6-2

MATH IN THE REAL WORLD 6-2 MATH ETIQUETTE 6-1

MATH ETIQUETTE 6-1 PRACTICE THE SKILL 6-1

PRACTICE THE SKILL 6-1 PRACTICE THE SKILL 6-2

PRACTICE THE SKILL 6-2 PRACTICE THE SKILL 6-3

PRACTICE THE SKILL 6-3 MATH IN THE REAL WORLD 6-3

MATH IN THE REAL WORLD 6-3 PRACTICE THE SKILL 6-4

PRACTICE THE SKILL 6-4 Look over your answers. Do they make sense? Most errors occur because of inaccurate math computations.

Look over your answers. Do they make sense? Most errors occur because of inaccurate math computations. PRACTICE THE SKILL 6-5

PRACTICE THE SKILL 6-5